- GoldenGround

- Posts

- How Real Estate Investors Locate The Best Foreclosures in Any Market

How Real Estate Investors Locate The Best Foreclosures in Any Market

Insider Tips to Navigate the Foreclosure Market with Confidence

Vlad Shostak

July 14, 2024

How Real Estate Investors Locate The Best Foreclosures in Any Market

Last updated: July 2024. The following is not financial advice; always do your own research.

When I got into real estate I thought foreclosures were the best way to get a good deal. I was wrong and I was right… there are many ways to find a good deal and each one has its set of problems.

Before diving deep into how to find good deals on foreclosures, we have to know at which point of the foreclosure we can get the best deal.

For example, getting a deal done at the pre-foreclosure stage can be more advantageous than waiting for it to go to auction… if you can solve for the obstacles attached with this approach (which we cover at the end of this article).

First the process.

The foreclosure process

Payments are missed…

-> Notice of Default (NOD) — opportunity on a pre-foreclosure deal)

-> Foreclosure Auction — opportunity on a foreclosure deal)

-> REO (Real Estate Owned) after not selling — opportunity on a foreclosure (but not so much in 2024)

In more detail:

1. Missed Payments

The homeowner misses one or more mortgage payments.

Lender attempts to contact the homeowner to resolve the issue.

2. Notice of Default (NOD)

After a specified period of missed payments (usually 90 days), the lender appoints a trustee (e.g. title company) (if non-judiciary state) and issues a Notice of Default (NOD).

The NOD is filed with the county clerk’s office and is a public record.

The NOD includes details of the missed payments and the total amount required to cure the default.

3. Pre-Foreclosure Period

Typically lasts for about 120 days.

Homeowner can cure the default by paying the overdue amount or negotiating with the lender.

Homeowner may sell the property, negotiate a loan modification, or pursue a short sale.

4. Notice of Sale (NOS)

If the default is not cured, the trustee issues a Notice of Sale.

The NOS is filed with the county clerk’s office, posted on the property, and published in local newspapers.

The NOS includes the date, time, and location of the foreclosure auction.

5. Waiting Period

Typically 21 days after the NOS is filed and published.

Provides a final opportunity for the homeowner to cure the default or take other action.

6. Foreclosure Auction

The property is sold at a public auction to the highest bidder.

The trustee handles the auction.

If the property is sold, the highest bidder receives the trustee’s deed to the property.

7. Transfer of Ownership

The winning bidder at the auction receives the trustee’s deed.

If the property does not sell at auction, it becomes REO (Real Estate Owned), meaning the lender owns the property and will sell it through traditional real estate channels.

How to find pre-foreclosures

There are companies that specialize in tracking them and provide foreclosure lists, I’ll show examples below.

But before that, let’s go over how we can find them ourselves manually to understand the process.

If you want to find pre-foreclosures manually, you will have to search for NODs posted at your county clerk. If they have a website you can search for trustee activity (more below).

👉 If you’re new, here’s the breakdown of the terms:

In non-judicial states, lenders appoint a trustee because it is a legal requirement in many states to have deed of trust, which includes a trustee.

Having a trustee also helps them manage the foreclosure process without having to worry about managing it themselves.

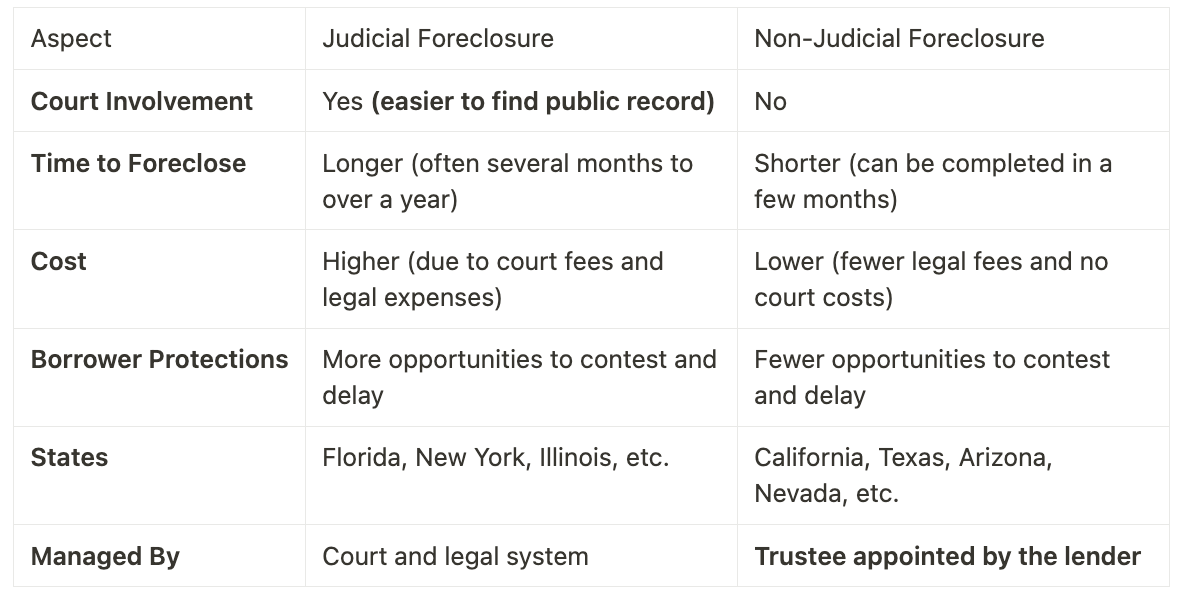

Judicial vs non-judicial states

Non-Judicial Foreclosure does not involve the court system, is faster and cheaper, but offers fewer protections for the borrower.

Some states and their statuses:

Arkansas: Both judicial and non-judicial foreclosures are allowed, but non-judicial is more common.

North Carolina: Primarily non-judicial foreclosure state.

Colorado: Allows both types, but non-judicial is more common.

Missouri: Permits both judicial and non-judicial foreclosures.

Who is the trustee

A trustee is an individual or organization appointed to manage the assets held in a trust.

In real estate, the trustee is a third-party company (title company/law firm/financial institution) that handles the foreclosure process on behalf of the lender.

The “trust” refers to a legal arrangement created by the deed of trust, which is a legal document that involves three parties in a real estate transaction:

Trustor (Borrower): The person buying the property who takes out the loan.

Beneficiary (Lender): The entity providing the loan.

Trustee: A neutral third party that holds the legal title to the property until the loan is repaid. If the borrower defaults, the trustee can sell the property to repay the loan without going to court in non-judicial states.

When a trustee comes in:

Default Notification: The homeowner defaults on their mortgage payments.

Lender Appoints Trustee: The lender (e.g., a bank like Wells Fargo) appoints a trustee (e.g., Quality Loan Service Corporation) to handle the foreclosure.

Notice of Default: The trustee prepares and files the Notice of Default with the county clerk’s office.

Trustee Manages Foreclosure: The trustee manages all subsequent steps (NOD, NOS, auction), including scheduling the foreclosure auction and ensuring compliance with legal requirements.

Finding pre-foreclosures manually - NODs from your County Clerk

As I mentioned, the documents related to foreclosure, such as the Notice of Default (NOD), are filed by the lender (bank, or mortgage company) or by the trustee (title company, law firm, or financial institution) acting on behalf of the lender.

Notices of Default and other foreclosure-related documents are filed with the county clerk and can be accessed online or at the courthouse.

For example:

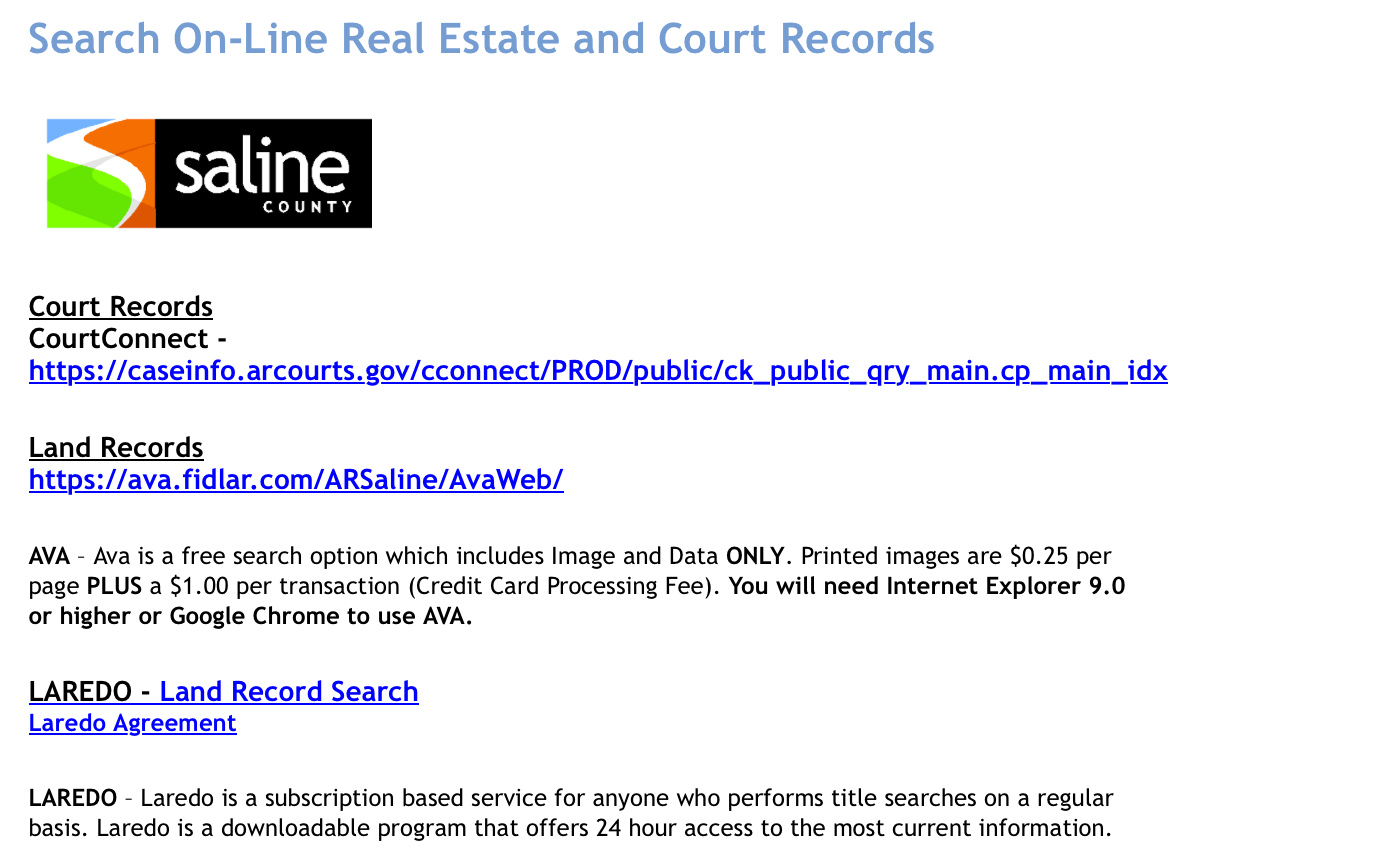

if I was looking at properties in Benton, Arkansas…

Benton is in Saline County, I can access foreclosure documents through the Saline County Circuit Clerk’s office.

Saline county, AR, County Clerk online property search.

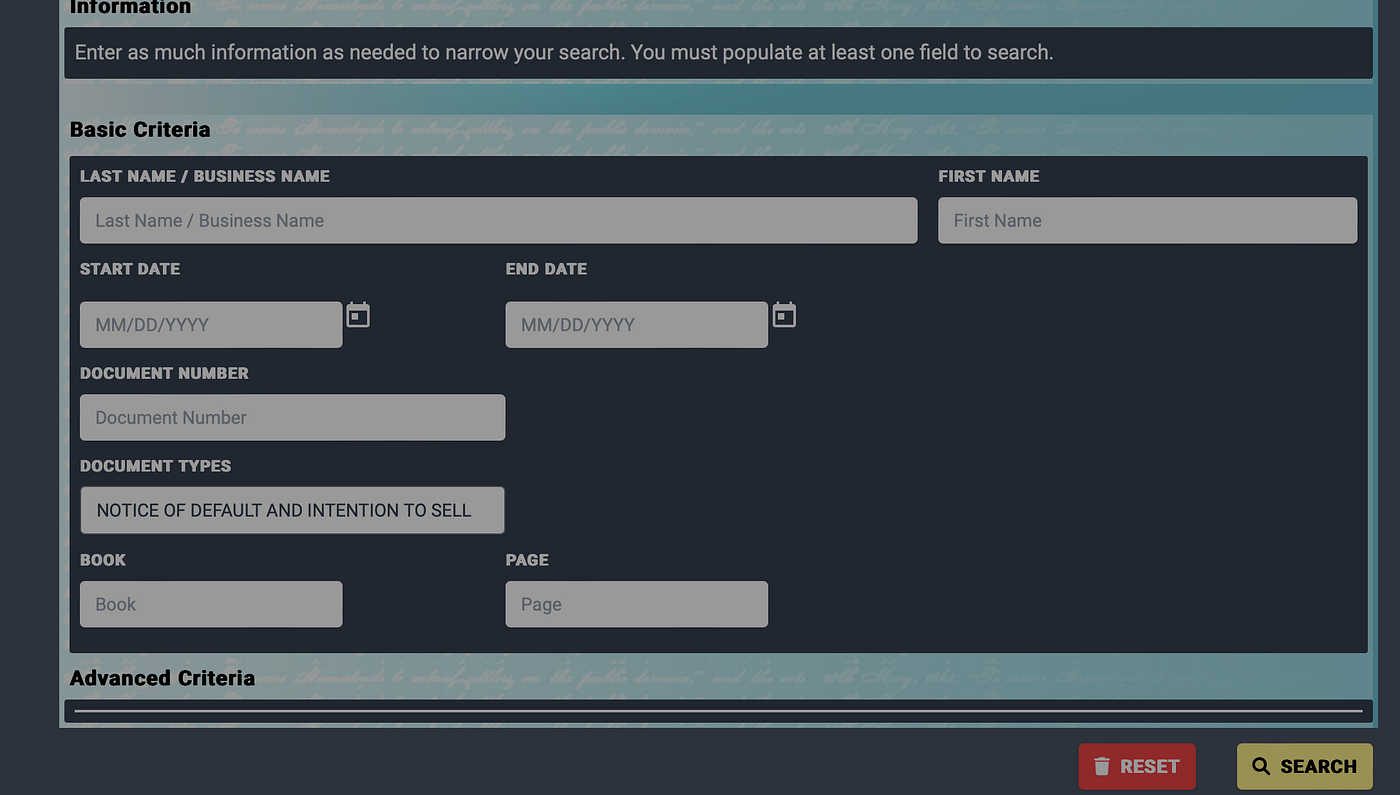

Searching Saline county clerk records

Do this for your county and visit in-person, some of them have NODs and NOSs posted on the wall.

Paid pre-foreclosure and foreclosure lists (best way)

Some companies provide lists of properties in pre-foreclosure or foreclosure.

Here are some of the best well known:

How to find regular foreclosures

#1 HomeSteps — Freddie Mac Homes

Freddie Mac is a government-sponsored enterprise (GSE), which means it’s a company created by the U.S. government to increase the availability of affordable housing.

Freddie Mac buys mortgages from banks and other lenders, then bundles them into securities and sells them to investors. This process helps to provide lenders with more money to make loans and ensures that there is a steady supply of funds for homebuyers.

#2 HUD Home Store — HUD Homes

HUD stands for the U.S. Department of Housing and Urban Development. It’s a government agency focused on national policies and programs that address America’s housing needs.

When a homeowner with an FHA-insured mortgage (a mortgage backed by the Federal Housing Administration, which is part of HUD) fails to make their mortgage payments and the home goes into foreclosure, HUD takes ownership of the property. The HUD Home Store is the website where HUD lists these foreclosed properties for sale.

#3 HomePath — Fannie Mae Homes

Fannie Mae is another government-sponsored enterprise (GSE), similar to Freddie Mac. It also buys mortgages from lenders, provides a steady source of funds for home loans, and helps make home buying more accessible.

When homeowners with mortgages backed by Fannie Mae can’t make their payments and the property goes into foreclosure, Fannie Mae takes ownership of the home. These properties are then listed for sale on the HomePath website.

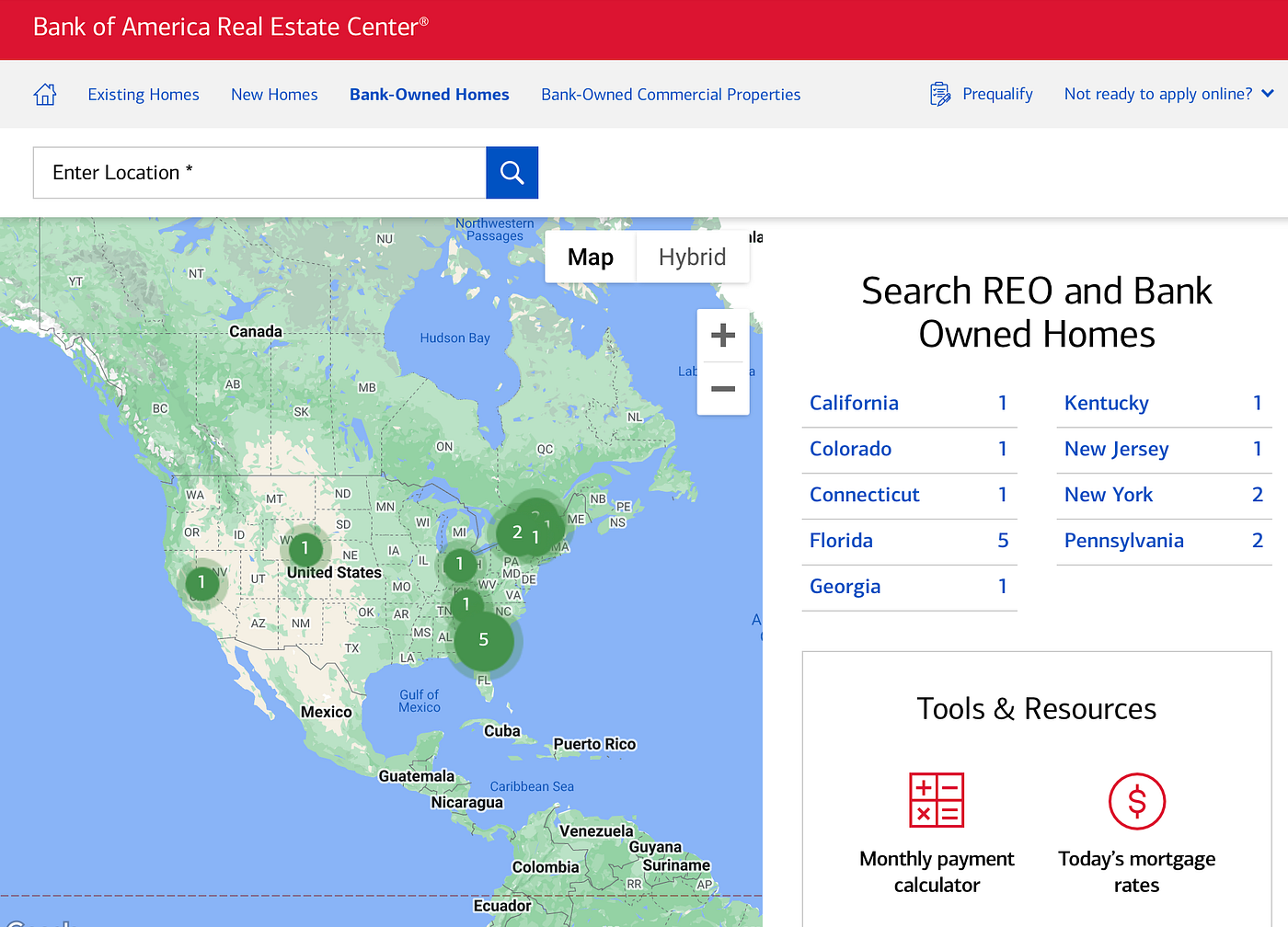

# 4 Big bank REO (Real Estate Owned) properties

These are homes that failed to sell at auction and are now owned by the bank.

If the foreclosed home fails to sell at auction, the ownership defaults to the original bank or lender.

On Google Search for:

“Bank of America Real Estate Owned”

“Chase bank owned properties”

Bank of America REO properties

# 4b Small or regional bank REO (Real Estate Owned) properties

These smaller banks might be more approachable and willing to provide you with a list of their foreclosed properties if you reach out to someone at the regional level, meaning someone who oversees a specific area or region.

Smaller banks you may have some luck reaching out to someone in at the regional level to see if they’ll give you access to the list.

#5 Network with your local experts (Obviously)

Form relationships with agents who specialize in foreclosures.

They may have access to exclusive listings and can provide insights into upcoming auctions and bank-owned properties.

Other sites (the mostly pull data from the ones above)

Before considering buying a foreclosure wouldn’t it be smart to understand the top 5 risks? I cover it HERE.

The problem with short selling pre-foreclosures

Foreclosure and pre-foreclosure deals require cash buyers or experts in short sales.

Creative financing isn’t an option since they’re already behind and likely underwater.

Short sales are usually a good bet. By the time properties reach foreclosure, they should already be approved for a short sale because the process can take longer than foreclosure.

PropertyRadar and similar services sell lead lists. Then, you need to knock on doors to find willing sellers.

The problem is that getting a short sale approved usually takes longer than the owner’s timeline.

Even if approved, securing a loan takes additional time. Finding leads is easy, but getting quick action from lenders is the challenge.

You might find a willing seller, but the bank could take 4 months to approve the short sale while the owner has only 120 days until foreclosure.

If you have cash, partner with realtors and let them know you’re ready for last-minute deals. Knowing the average timeline for foreclosures and short sales in your area will help you plan and act more efficiently.

Identify High-Yield Areas

The perfect place to buy a foreclosure is in a high-rental demand area with good schools, amenities and infrastructure development.

That is why it is important to research your local market trends in property values, rental rates, and economic indicators.

I cover this and more in my newsletter,

subscribe to stay updated on real estate trends and gain knowledge from the experts on real estate investing.